Very few companies are purely “green” or purely “brown”.

Most businesses operate across a mix of sustainable, transitional and legacy activities.

This creates a fundamental strategic question for boards and investors:

Which parts of the business actually create long-term sustainable value?

And how much of the firm’s enterprise value is driven by those activities?

Traditional valuation models rarely provide this insight. Companies are typically forecast as a single consolidated entity, or valued using a “sum-of-the-parts” approach based on legal entity structures.

Sustainability dynamics, however, rarely follow legal structures. Green, transitional and legacy activities often sit within the same business unit or product portfolio.

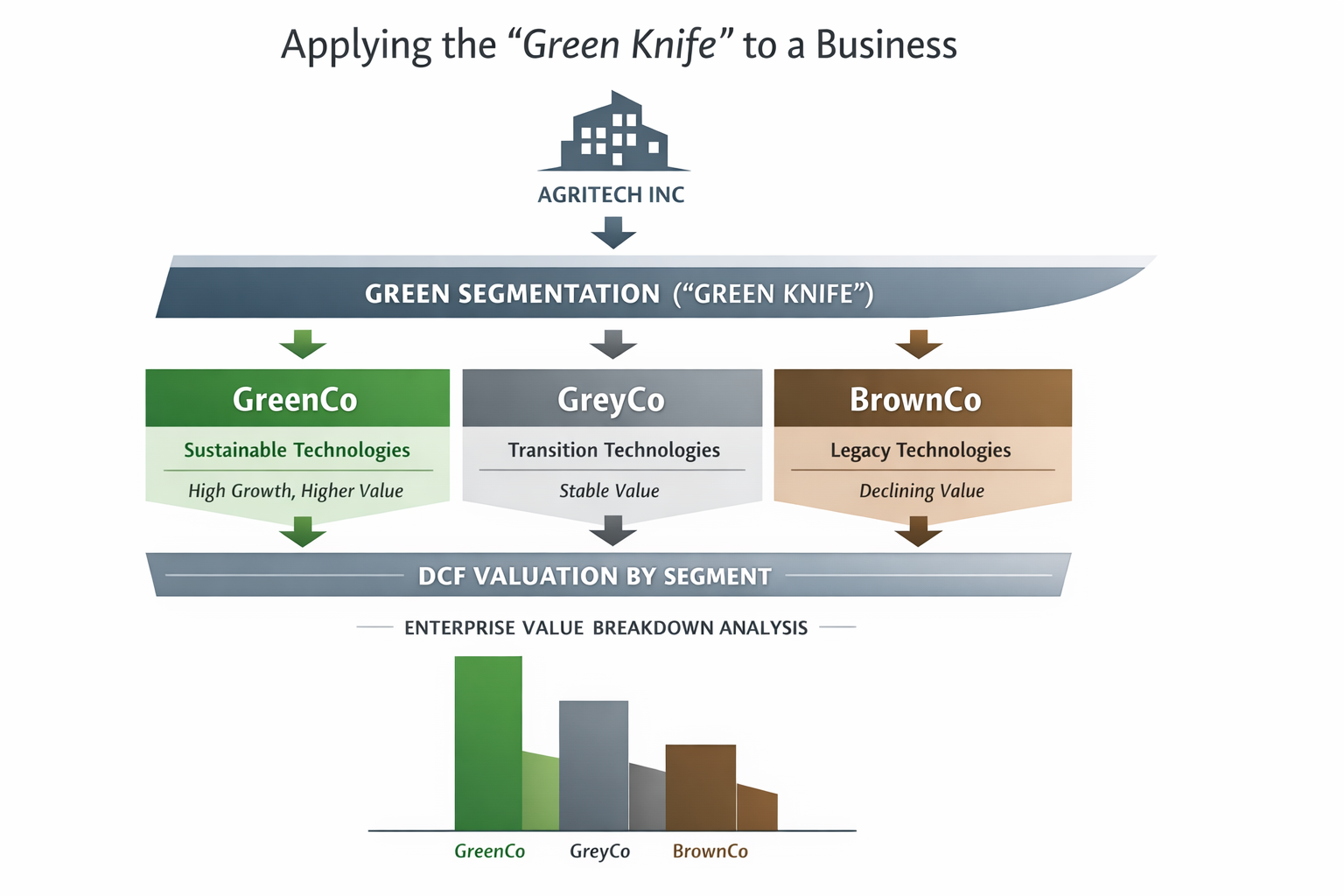

In this case study we highlight the approach of a green segmentation DCF model, developed by Sustainable Valuations. We refer to this approach as applying a “green knife” to the business — slicing the company along sustainability lines rather than legal or organisational ones.

Through the lens of a fictional greenhouse technology firm, we give a simplified view of the steps taken to uncover the green vs. brown components of a company’s value.

The Subject: A Greenhouse Technology Supplier

“Agritech Inc” designs equipment used in modern greenhouses. The company operates in a sector undergoing rapid technological change as growers look to truly put the “green” in greenhouse — reducing energy consumption while optimising water and nutrient use.

The firm’s product portfolio spans multiple technologies ranging from energy-intensive legacy systems to advanced sustainable solutions.

Using our green segmentation framework, we work with management to divide the business into three sustainability segments:

- GreenCo – Technologies that support the operation of largely climate-neutral greenhouses

(e.g. LED lighting, solar integration, precision irrigation, climate software) - GreyCo – Technologies that improve efficiency but are not yet carbon neutral

(e.g. ventilation systems, climate control equipment) - BrownCo – Legacy technologies associated with higher fossil fuel usage

(e.g. gas-based heating systems, traditional lighting)

Determining where products fall requires dialogue with management and the use of sustainability metrics such as carbon intensity, energy consumption or regulatory exposure.

Step 1 — Establish Three Economic Business Units

Although these entities do not exist legally, they function in the model as three internal subsidiaries.

The first step is to derive simplified financial statements for each segment by allocating key financial line items, including:

• revenue

• cost of goods sold (COGS)

• fixed operating costs

• operating assets

Where sufficiently granular information exists (for example product-level sales), a bottom-up approach is used.

Where data is less granular (such as shared operating costs), we apply an allocation methodology, for example:

• allocation based on revenue share

• allocation based on operational drivers

• or a manual sustainability overlay reflecting structural differences between business lines

For example, GreenCo might generate 45% of revenues but require 50% of production costs if its technologies rely on more expensive materials or engineering effort.

Table 1 – Starting Business Allocation

| Business Line | Example Products | Revenue Share |

| GreenCo | LED lighting, precision irrigation, climate software | ~45% |

| GreyCo | greenhouse structures, ventilation systems | ~30% |

| BrownCo | gas heating systems, legacy lighting | ~25% |

Step 2 — Forecast Each Segment Independently

Once Agritech’s current financials have been segmented, we turn to the future.

Management forecasts should not only be challenged — they should also be split across the three sustainability segments.

Given the longer time horizon of sustainability transitions, the model uses a nine-year forecast period, divided into:

• short term (years 1-3)

• medium term (years 4-6)

• long term (years 7-9)

After this period the valuation transitions into a terminal value.

Table 2 – Segment Growth Outlook

| Segment | Short-Term Growth | Medium-Term Growth | Long-Term Growth | Strategic Interpretation |

| GreenCo | 7% | 5% | 3% | rapid adoption of automation and energy-efficient technologies |

| GreyCo | 4% | 2% | 2% | stable replacement demand |

| BrownCo | –3% | –4% | –5% | gradual phase-out of legacy heating systems |

Investment behaviour also evolves differently across the segments:

• GreenCo invests in innovation and growth

• GreyCo maintains installed infrastructure

• BrownCo gradually reduces investment as demand declines

Step 3 — Translate Forecasts Into Cash Flow

Operational forecasts are then translated into expected cash flow streams for each segment.

In principle, each segment could have its own cost of capital reflecting different risk profiles and sustainability exposure.

In this illustrative example we maintain a single company-level discount rate, allowing the analysis to focus on how operational differences drive value across the segments.

Step 4 — The Valuation Results

Applying this framework to Agritech produces the following valuation breakdown.

Table 3 – EV split by segment

| Segment | Enterprise Value | Share of Total |

| GreenCo | €29m | 53% |

| GreyCo | €9m | 16% |

| BrownCo | €17m | 31% |

| Total Enterprise Value | €55m |

In this case, the company’s green activities already represent more than half of enterprise value, reflecting stronger expected growth and long-term demand for sustainable greenhouse technologies.

However, transitions are rarely linear. Regulation, technology innovation, energy prices and customer demand all influence how quickly value shifts from legacy to sustainable activities.

How to Use the “Green Knife” Valuation

Beyond valuation itself, this type of analysis can help management teams think more clearly about the sustainability transition taking place inside their business.

Segmented sustainability valuation can support decisions around:

• capital allocation across product lines

• product development and innovation priorities

• acquisitions or divestments

• sustainability strategy

• investor communication

Understanding which activities drive long-term value can be critical when navigating technological transitions.

In Short

As industries transition toward more sustainable technologies, many companies will operate mixed portfolios of green, transitional and legacy activities for years to come.

Traditional valuation models often overlook this complexity.

Segmented valuation provides a practical framework to understand how different parts of the business contribute to enterprise value — and how that balance may evolve over time.

In the case of Agritech Inc., the analysis shows that while green technologies are already the largest contributor to value, the company’s transition remains very much a work in progress.

For investors and management teams alike, understanding where sustainability value is created inside the firm will increasingly become a core element of strategic financial decision-making.